This article is the first entry in The Breach’s ‘Racism and Housing Series,’ an ongoing investigation into how systemic racism is shaping the housing crisis across Canada. Read part two here.

Across Canada, real estate developers and big corporate landlords are systematically exploiting racialized communities, buying up properties where they live at low prices and then flipping them for profit—after evicting long-term residents.

A new report, obtained exclusively by The Breach, shows that this practice is not incidental but a nationwide tactic employed by “financialized landlords.” These are entities like real estate investment trusts (REITs), asset managers, and pension funds that treat rental housing as an investment to generate shareholder profits, rather than a place for people to live.

The strategy hinges on a discriminatory and cynical assumption: removing Black and Arab tenants reliably raises property values and unlocks new profits.

These landlords methodically target buildings with low rents and long-standing, mostly immigrant tenants. Through capital upgrades, neglect, or renovation-driven evictions—what the industry euphemistically calls “repositioning”—they displace current residents and convert the housing into higher-value assets.

Across Canada’s largest cities, these practices are intensifying the housing crisis, driving rents up, and eroding social cohesion in neighbourhoods already struggling with affordability.

The mechanics of the ‘racial dividend’

At the centre of this national phenomenon is what Dr. David Wachsmuth, Canada Research Chair in Urban Governance at McGill University, calls the “racial dividend.” His research, conducted with Nora Ottenhof of Toronto Metropolitan University and Inez Hillel of Vivic Research, set out to measure the relationship between the racial makeup of a neighbourhood and its real estate values, and to trace how landlords exploit it.

They prepared the report as expert evidence for the Ontario Human Rights Tribunal in the case Yussuf et al. v. Timbercreek Asset Management. Still ongoing, the case stems from the 2018 mass eviction of more than 500 residents from Ottawa’s Heron Gate community, where mega-landlord Timbercreek demolished 150 townhouses, displacing a predominantly immigrant and racialized population.

The tenants at Heron Gate, 90 per cent of whom are people of colour, allege that Timbercreek (which later rebranded as Hazelview) deliberately targeted their neighbourhood to attract a “predominantly affluent, white, and non-immigrant community” in its place.

Wachsmuth and his co-authors’ research raise the prospect that systemic racial targeting is not just a bug in the system of financialized housing, but a feature of how the business operates.

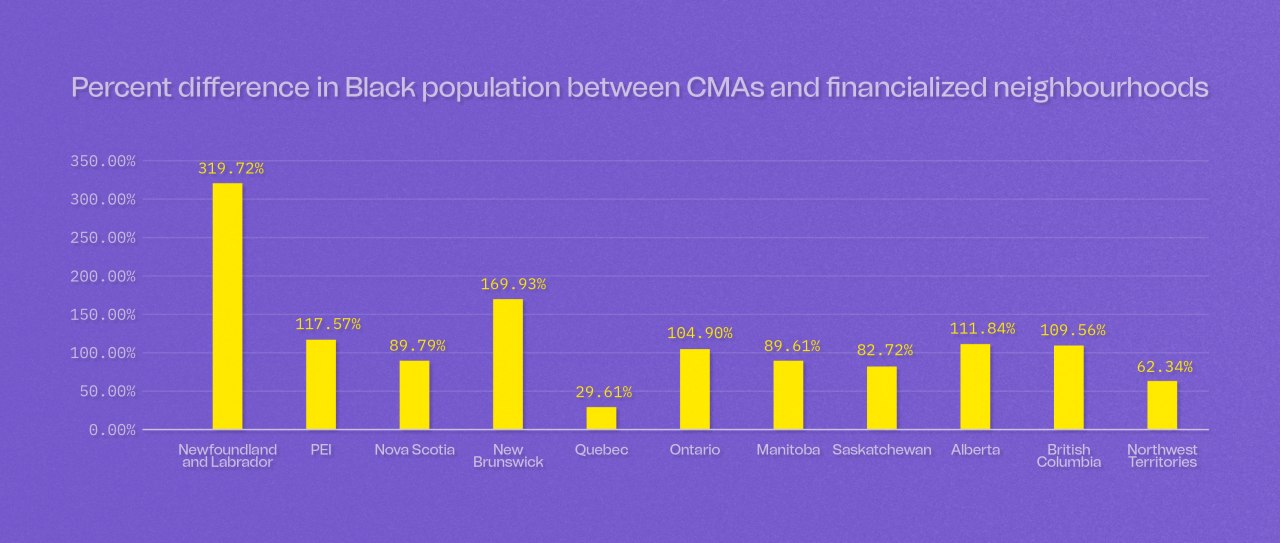

According to their findings, across Canada’s six largest cities—Toronto, Montreal, Vancouver, Edmonton, Calgary, and Ottawa—neighbourhoods with higher concentrations of African, Caribbean, and Middle Eastern residents consistently see lower property value growth than comparable, predominantly white areas.

The report analyzed more than 2,800 census areas across these metropolitan regions using Statistics Canada’s 2006 and 2016 census data. This was the same decade of information available to investors like Timbercreek when its redevelopment plans spurred the large-scale evictions in Ottawa. Its regression models controlled for income, housing type, education, and proximity to city centres, confirming that race and ethnicity alone predict slower property appreciation.

According to the report, “The patterns observed in the analysis point to market mechanisms that create financial incentives for developers to target racialized neighbourhoods for redevelopment and demographic change.”

The authors identify two mechanisms that, taken together, generate this racial dividend. First is the “race discount”: the suppressed property values that allow developers to acquire buildings cheaply in racialized areas. Second is the “race bonus”: the profits unlocked when those tenants are evicted, wealthier and whiter residents move in, and values rise without meaningful improvements or additions to the housing stock.

The quantitative evidence is eye-opening. A one-percentage-point increase in the share of Caribbean or Middle Eastern residents in a neighbourhood is associated with a $13,640 drop in housing value growth between 2006 and 2016. For African immigrants, the penalty is more severe: every one-percentage-point increase in their share of a neighbourhood’s population is linked to a $144,630 drop in property value growth.

In Heron Gate itself, the share of Caribbean, African, and Middle Eastern residents more than doubled between 2006 and 2016—from 25 to 55 per cent—while property values grew just 6.9 per cent, compared to nearly 50 per cent across Ottawa as a whole.

“Racialized neighbourhoods are being targeted for a particularly predatory form of development by financialized landlords, and we can prove it,” said lawyer Daniel Tucker-Simmons, who is representing former residents of Heron Gate in the human rights complaint.

“Through meticulous quantitative analysis, our experts have been able to compare areas and properties that are similar in all material respects except for the racial composition of the residents. These comparisons have then allowed us to conclude that housing prices are negatively correlated with higher concentrations of racialized people, especially Black tenants. Ergo, rental buildings in racialized and Black neighbourhoods can be acquired at a discount, increasing profit potential and making them more attractive for acquisition by financialized landlords.”

For financialized landlords, this becomes a business model. They acquire undervalued buildings in racialized enclaves, carry out selective renovations or strategic neglect, and then raise rents once long-standing tenants are displaced.

Many of these buildings sit near wealthier, whiter neighbourhoods, making them prime targets for speculative redevelopment.

Engineering displacement for profit

Landlords claim that when tenants are displaced from overwhelmingly racialized, immigrant, and low-income neighbourhoods, it’s just “the market at work.” But evidence suggests that it’s a deliberate strategy. The Competition Bureau is currently investigating major landlords for alleged high-tech rental price-fixing through software such as YieldStar, an algorithm that aggregates confidential rent data from property managers to recommend coordinated rent increases across urban housing markets.

This means corporate landlords are colluding to actively shape markets, using shared data and pricing tools to close “rent gaps” and drive up returns in lockstep. By evicting long-time tenants paying below-market rents, they can jack up prices (often hundreds or even thousands of dollars higher) leaving displaced tenants unable to afford comparable housing nearby.

The impacts are often devastating. Families rooted in these communities for decades are forced out, with few options beyond moving to overcrowded units, doubling up with relatives, or leaving the city entirely.

As the Wachsmuth report shows, this process is not race-neutral: property values are closely tied to neighbourhood racial composition. When an area is home to a visible concentration of Black, Arab, or other racialized residents, it is perceived by investors as devalued real estate. That devaluation creates a perverse incentive whereby the very presence of racialized tenants signals an opportunity for profit-maximization.

Developers exploit these lower land values to acquire buildings cheaply, displace those same communities, and then revalue the area through demographic turnover rather than actual improvements to the housing stock.

These kinds of “renovictions” are the industry’s most effective tool for displacement. It works precisely because it operates under the veneer of legality. Landlords in Ontario, for example, use the province’s N13 eviction notice system, which allows them to remove tenants for “extensive renovations,” demolitions, or conversions to other uses. On paper, tenants have a “right to return” to their unit once the work is complete, but in reality, this rarely happens.

Instead, landlords rely on a combination of legal and extra-legal tactics to ensure tenants leave for good: buyout offers, ignored repair requests, and months of disruptive construction that make homes unlivable. Once a tenant accepts an offer or moves out, the landlord can quickly re-rent the unit at double or triple the previous rate.

The process is technically lawful, yet it effectively weaponizes the Residential Tenancies Act against long-term renters—especially those with limited resources or awareness of their rights—turning what should be a protective measure into a tool for displacement.

Earlier research that Wachsmuth did in 2023 for the Canada Mortgage and Housing Corporation adds another layer to this picture, showing how eviction functions not just as a by-product of poverty, but as a cause of it.

Interviews with tenants across four provinces found that forced moves often triggered lasting social and economic collapse: loss of income and community ties, and in many cases, homelessness.

Racialized and Indigenous tenants were four times more likely than white tenants to report sudden rent hikes or eviction notices, and nearly twice as likely to end up in transitional or unstable housing afterward.

These findings confirm that eviction is not merely a local misfortune but a predictable outcome of the financialized housing model. The power imbalance between landlords and tenants, particularly in corporate-owned buildings, gives firms near-total control over who stays and who goes.

Financialized landlords are contributing to a national housing crisis

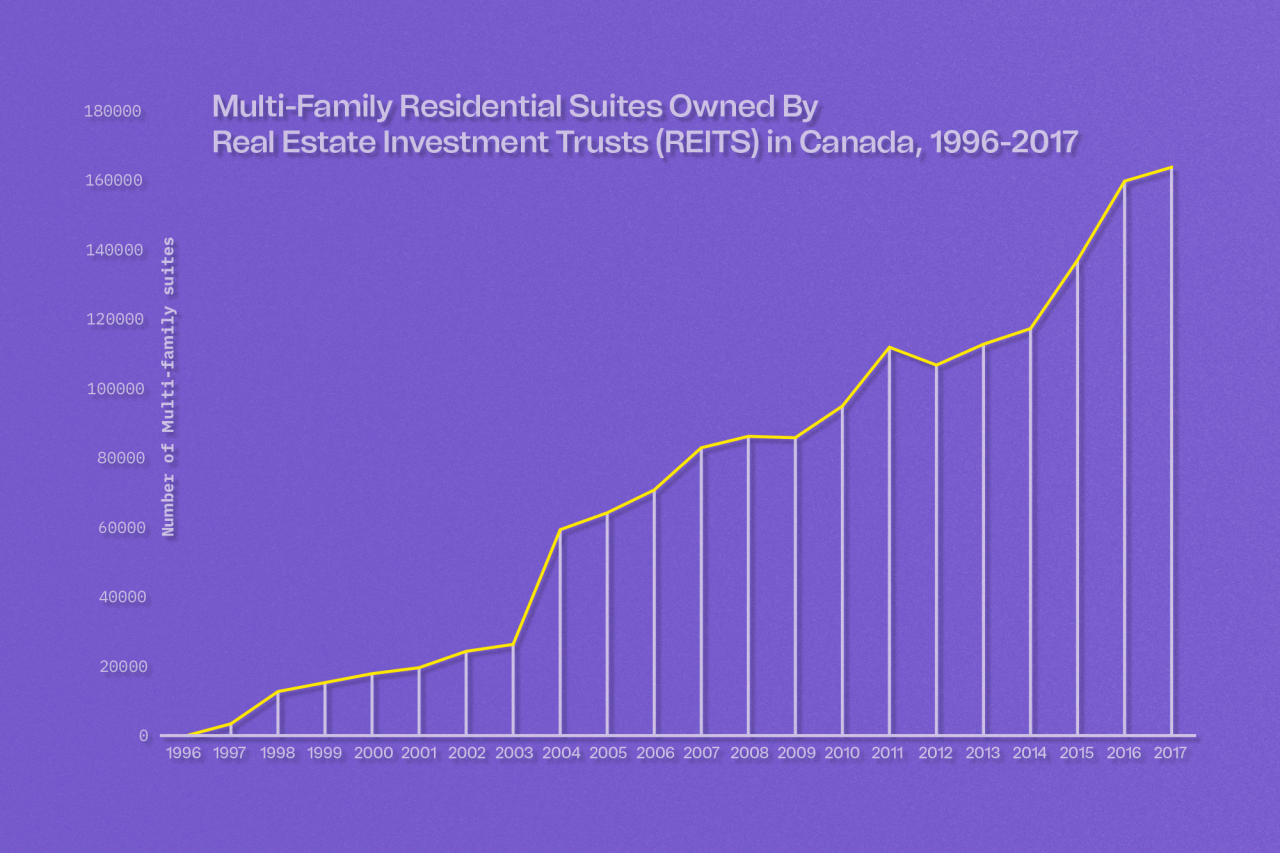

The corporate takeover of Canada’s rental market is part of a larger shift: the investor-focused rise of financialized landlords and REITs. In 1997, financialized landlords owned virtually none of Canada’s multi-family rental stock. Today, they control 20 per cent nationwide.

CAPREIT, the largest publicly traded apartment landlord in Canada, holds over $14 billion in assets and owns over 45,000 rental units and townhomes domestically. The American giant Blackstone controls approximately $20 billion of Canadian property alone.

The implications of this shift are profound. Financialized firms are legally exempt from corporate taxes as long as profits are distributed to investors. This incentivizes a relentless focus on maximizing quarterly returns, often through rent increases and evictions, rather than maintaining or building new affordable housing stock. For tenants, this often means frequent evictions, rent hikes, and worsening conditions.

According to Ricardo Tranjan, research director at the Ontario office of the Canadian Centre for Policy Alternatives and one of the country’s leading housing experts, the explosion of financialized housing is no accident.

“Throughout Canadian history, private developers and landlords took advantage of various crises to enrich themselves,” he said. “The property-owning class’s impetus to exploit the universal need for shelter is a constant.”

The roots of this financialization run deep in Canada’s economic policy. In 1997, the federal government quietly changed the rules governing the Canada Pension Plan Investment Board (CPPIB), lifting restrictions that had previously limited pension fund investments to public infrastructure. That change, followed by 2005 reforms that removed caps on foreign investment, opened the floodgates for pension funds to invest in private equity, infrastructure, and real estate.

Today, housing is part of an emerging “asset manager society” where the state has retreated from public or non-market housing provision, tenant protections have been eroded, and rules protecting tenants have been stripped away.

“Several factors contributed to this trend, including the global shift toward capital deregulation, but I always like to highlight that weak rent controls are a key enabler of profiteering in rental housing,” said Tranjan. “Vacancy controls and strict eviction laws make apartment buildings a lot less attractive to aggressive investors, as ‘repositioning’ them is not as easy.”

Indeed, financialized housing works like a high-yield investment: the more quickly and extensively tenants can be displaced, the higher the profits. Between 2011 and 2021, Canada lost 15 affordable homes for every new one created.

The evidence is mounting: a combination of racialized targeting, financialization, and lax regulation has created a housing system that is increasingly extractive, unstable, and discriminatory. Black and brown communities are being uprooted to make way for wealthier tenants, while financialized landlords reap enormous profits.

The Heron Gate case is a litmus test of whether the courts and regulatory system will recognize and condemn a business model that uses race as a line item in profit calculations.

If the Tribunal agrees with the Heron Gate tenants—that large landlords systematically treat properties in racialized neighbourhoods differently—the resulting legal record could reshape how policymakers, housing advocates, and the public understand the mechanics of financialized housing. It could mark a shift from reactive, after-the-fact responses to proactive, systemic regulation.

This could mean reintroducing nationwide rent controls, massively expanding the stock of non-market and public housing, and strictly regulating financialized landlords as a class of service providers responsible for defined social as well as economic outcomes.

Only by treating housing as a social good, not merely a financial asset, can Canada begin to address the dual crises of affordability and racialized displacement.

“It’s about getting to the bottom of things. It’s about unveiling who has the power and what they’re doing with that power.”

Linda McQuaig, journalist and author

As a non-profit, free from powerful corporate interests, we invest in investigations and uncover the cover-ups. Sustain our journalism for transformation.

Housing | Canadian mega landlord using AI ‘pricing scheme’ as it massively hikes rents

Housing | How Canada’s media manufactures sympathy for the landlord class

‘Nightmare’ landlord greenwashes move to displace low-income tenants

3 comments

Comments are closed.

“Developers exploit these lower land values to acquire buildings cheaply, displace those same communities, and then revalue the area through demographic turnover rather than actual improvements to the housing stock.”

Very interesting article that begs the question “why”. Why are racialized neighborhoods lower valued than primarily white neighborhoods, if the housing is relatively the same?

Great story but where can I get the actual report detailing the financialized landlords targeting black and arab neighbourhoods?

Hello: In my opinion, necessary changes to Canada’s (housing rental-laws) could include: Requiring that Canadian Lease-Agreements stipulate that Landlords & Tenants uphold the Charter & Criminal Code during the Lease-period, enacting “Reward for Good Behaviour-” initiatives, in which funding is given to Landlords wanting to try a pilot project in which their Tenants are tasked with completing volunteer work, in the surrounding community, that supports causes held dear by the Landlord, & enacting a new Criminal Code-infraction, the “Good Samaritan Law,” meaning that Canadian citizens must report & disclose unsafe situations, such as in the case of a Landlord who evicts a Tenant without compelling evidence or inarguable reasoning, something that could put the Tenant at risk of being unhoused &, in turn, with dire threat to his/her security, which could extend as far as threatening the continuation of a human life. I think any Landlord found in contravention of my hypothetical “Good Samaritan Law” should be charged criminally. Furthermore, efforts could be made to make it easy for Tenants to unionize, & in the case of a Tenant Union forming, it may be found to discourage poorish Landlord-behaviour. Thank you for publishing the article! -Renee K. Taylor, BA (French;) Kamloops, BC (Oct. 27/25.)